Getting a foreclosure notice feels like the floor has dropped out from under you. One minute, you own a home, and the next, a letter says you could lose it all. Here is the thing most people do not know: receiving that notice is not the end. It is actually the beginning of a window where you can still fight back. If you are behind on mortgage payments in Tampa, you are not alone, and you have more options than you think.

Whether you just missed a payment or you are weeks away from a sale date, this guide breaks down 10 real, proven ways to protect your home. And if you have been searching for ways to sell my house fast in Tampa, FL, we cover that too.

What Is Florida’s Foreclosure Process?

Florida is a judicial foreclosure state. Your lender must take you to court before selling your home. The full process typically takes 6 to 18 months, from the first missed payment to the auction. That timeline is your window to act.

The basic steps:

- You miss 3 or more payments

- The lender files a lawsuit in the Hillsborough County court

- You have 20 days to respond to the summons

- A judge rules on the case

- The sale date is set if the ruling goes against you

- Home is auctioned at the courthouse

Every step is an opportunity to negotiate, apply for help, or sell on your terms.

What Are the 10 Ways to Stop Foreclosure in Tampa, Florida?

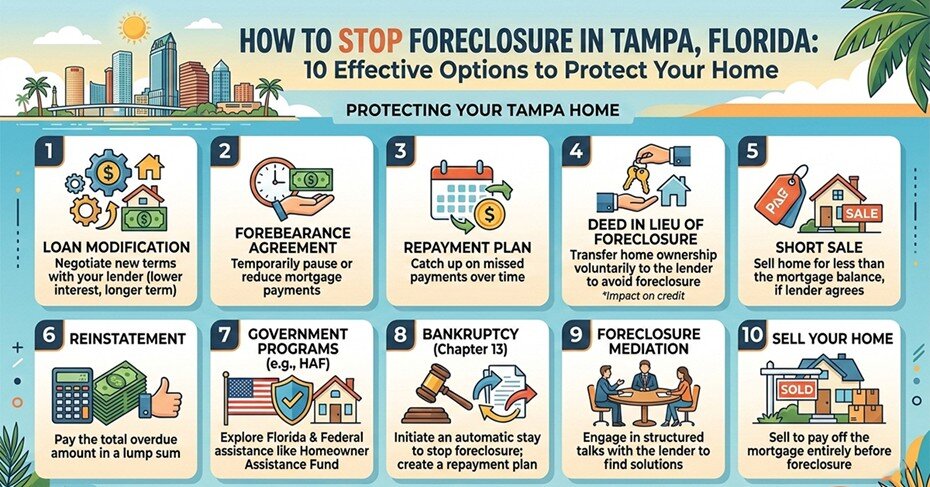

Option 1: Call Your Lender Before Anything Else

Call before you do anything else. Ask for the “loss mitigation” department. Have your loan number, last two pay stubs, two months of bank statements, and a brief hardship explanation ready. Lenders would rather work out a deal than go through an expensive foreclosure.

Option 2: Apply for Forbearance

Forbearance pauses or reduces your payments for 3 to 12 months. You still owe the money, but it buys time during a job loss, illness, or other short-term hardship. Contact your loan servicer directly to apply.

Option 3: Set Up a Repayment Plan

If your income has recovered, ask your lender for a structured repayment plan. You pay your regular monthly amount plus a little extra each month until you are caught up. Most plans run 3 to 12 months.

Option 4: Request a Loan Modification

A loan modification permanently changes your mortgage terms. Your lender may lower your interest rate, extend your loan term, or roll missed payments into your balance. Ask your servicer for a “loan modification hardship application” to start the process. It typically takes 30 to 90 days.

Option 5: Get Help from a Free HUD-Approved Housing Counselor

This is the most underused resource in Tampa, and it costs you nothing. HUD-approved housing counselors can help you figure out your options and guide you through the paperwork and process of working with your servicer. Help is free. You do not have to pay anyone to help you avoid foreclosure.

How to find a free HUD counselor in Tampa:

- Call: 800-569-4287 (HUD’s national hotline)

- Visit: hud.gov to search for HUD-approved agencies in Hillsborough County

- Housing and Education Alliance (HEA): A Tampa-based nonprofit that specifically helps homeowners facing foreclosure. They are HUD-certified and serve Hillsborough County directly.

A counselor will review your entire financial picture, contact your lender on your behalf, and help you apply for assistance programs, all at no charge.

Option 6: Apply for State Assistance

Florida received $676 million through the federal Homeowner Assistance Fund (HAF) to help homeowners cover missed mortgage payments, property taxes, and insurance. Check current program availability at FLHomeownerAssistance.org or call 833-987-8997 for current status before applying, as funds are limited.

Option 7: Refinance Your Mortgage

If you have equity and your credit score is still intact, refinancing into a lower rate can reduce your monthly payment enough to get current. This option works best early, before multiple missed payments have damaged your credit.

Option 8: Pursue a Short Sale

A short sale means selling the house before foreclosure for less than what you owe. Your lender accepts the sale price as full payment and forgives the rest. It damages your credit far less than a completed foreclosure, and it gives you control over the outcome. Lender approval is required before listing.

Option 9: Deed in Lieu of Foreclosure

You voluntarily return the home to your lender, and they cancel your remaining mortgage debt. You lose the property, but you avoid a court judgment and reduce long-term credit damage. Ask your lender specifically whether this is an option for your loan.

Option 10: Sell for Cash Before the Auction

Selling the house before foreclosure to a cash buyer is the fastest way to stop the process entirely. Unlike a traditional listing, which can take 60 to 90 days in Tampa, a cash sale can close in 7 to 14 days. The sale pays off your mortgage, stops the foreclosure, and may leave money in your pocket. If you need to sell my house fast in Tampa, FL, this is the cleanest option when time is critical.

FAQs

Q.1) How long does the foreclosure process take in Florida?

Florida’s judicial foreclosure typically takes 6 to 18 months from the first missed payment. This gives homeowners significant time to negotiate with lenders, apply for assistance, or explore selling options before losing the home.

Q.2) Can I stop a foreclosure the day before the sale in Tampa?

In many cases, yes. Filing for bankruptcy triggers an immediate automatic stay that pauses the sale. Paying the full past-due amount (called “right to cure”) can also stop it. Contact a foreclosure attorney or HUD counselor right away.

Q.3) Will selling my house stop foreclosure?

Yes. If your home sale closes before the auction date, the proceeds pay off your mortgage, and the foreclosure stops completely. A cash buyer can often close in 7 to 14 days, making this one of the fastest solutions available.

Q.4) Does foreclosure affect my credit score?

Yes. A completed foreclosure can drop your credit score by 100 points or more and stay on your report for 7 years. Options like loan modification, a short sale, or a fast cash sale cause significantly less long-term credit damage.

Q.5) What happens if I just stop paying and do nothing in Florida?

Doing nothing leads to a completed foreclosure and possibly a deficiency judgment. That means the lender can sue you for the difference between what you owed and the auction sale price. Always pursue a formal resolution to protect yourself legally.

Ready to Stop Foreclosure Fast? Here Is How We Can Help

If you are running out of time, we want you to know there is still a path forward. At Tampa Fast Home Buyer, we work directly with homeowners across the Tampa Bay area who need a fast, fair, and hassle-free sale. We buy homes in any condition, with no repairs required, no agent commissions, and no waiting around for a buyer’s loan to be approved.

Whether you are exploring selling the house before foreclosure to protect your credit or you simply need to sell your house fast in Tampa, FL, we can close in as little as 7 days on a timeline that works for you. You pick the closing date, we handle all the paperwork, and you walk away with cash and peace of mind. Do not let the bank control the outcome of your story. Take the first step today at tampafasthomebuyer.com.